The wealth management industry is experiencing a fundamental shift in how firms serve clients. Revolve Wealth Partners represents one approach in this evolving landscape, offering lessons for investors seeking partners who can navigate increasingly complex financial markets. Understanding what defines effective wealth management today helps you make better decisions about who manages your capital.

The Traditional Wealth Management Model and Its Limitations

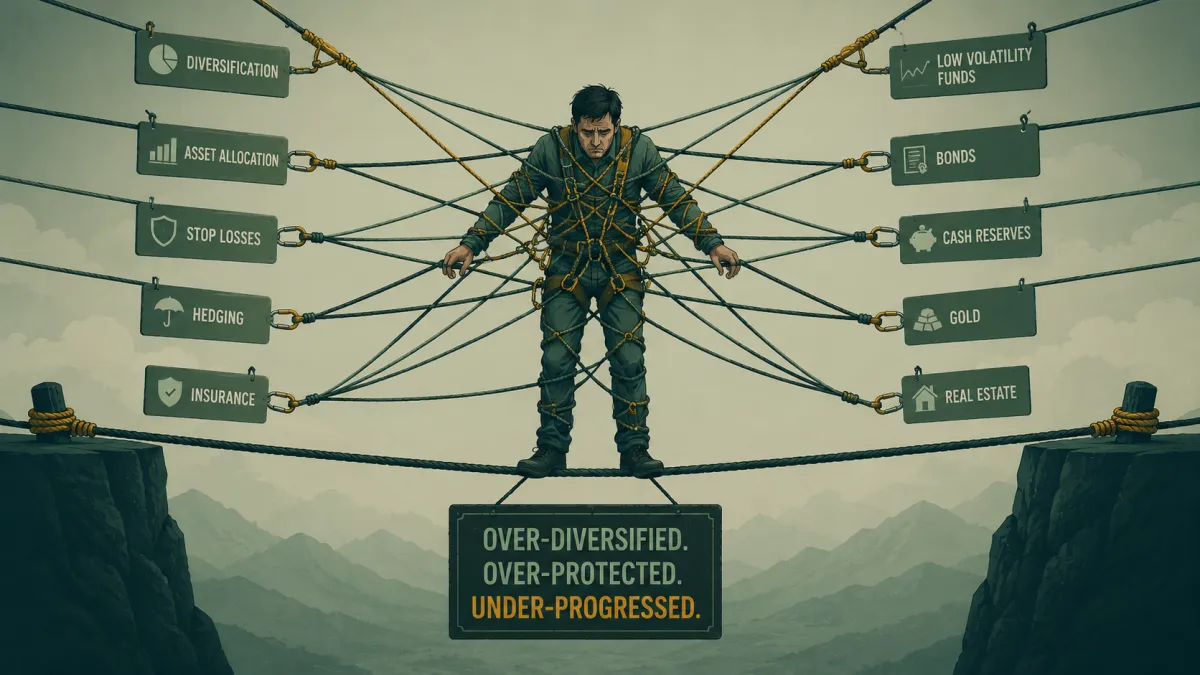

Most wealth management firms follow a predictable pattern: diversified portfolios, passive index funds, and the promise that patience wins over decades. This model worked when inflation stayed below 3% and markets trended predictably upward. Today's environment demands different thinking.

Revolve Wealth Partners emphasizes a client-centric approach, which represents growing awareness in the industry that cookie-cutter solutions no longer serve ambitious investors. When Paul Tudor Jones famously said he never invests in anything he doesn't understand completely, he highlighted a principle many traditional advisors ignore: your wealth manager should match strategies to your actual goals, not industry standards.

Why Generic Portfolio Allocation Falls Short

The typical 60/40 stock-bond allocation has delivered diminishing returns since 2020. Bond yields barely keep pace with inflation, and stock valuations remain historically elevated. Yet many firms continue recommending these allocations because they're simple to implement and easy to justify.

Consider the experience of Tony Robbins, who discovered through interviewing top investors that the ultra-wealthy use fundamentally different strategies than what retail investors receive. His research revealed that billionaires focus on asymmetric returns - opportunities where downside is limited but upside is substantial.

Key problems with traditional allocation:

- Assumes all clients have identical 30-year time horizons

- Ignores current market valuations and economic cycles

- Treats inflation as a minor consideration rather than a wealth destroyer

- Provides identical advice regardless of whether markets are expensive or cheap

What Differentiates Modern Wealth Management Firms

Examining firms like revolve wealth partners reveals several characteristics that separate forward-thinking advisors from those stuck in outdated models. Evolving client expectations now emphasize transparency, active risk management, and alignment of interests.

| Traditional Approach | Modern Approach | Impact on Returns |

|---|---|---|

| Annual rebalancing | Active monitoring | Captures opportunities, limits losses |

| Passive index exposure | Strategic positioning | Adapts to market conditions |

| Generic risk tolerance | Customized risk profiles | Matches actual goals |

| Quarterly reports | Real-time access | Informed decision-making |

Ray Dalio built Bridgewater Associates on the principle that diversification without active management is "financial suicide" in his words. His all-weather portfolio concept emphasizes understanding economic environments and positioning accordingly - not simply buying and holding through all conditions.

The Transparency Revolution

Clients increasingly demand clarity about what they own, why they own it, and how fees impact returns. The days of vague explanations and hidden costs are ending. Revolve wealth partners and similar firms now face pressure to justify every position and decision.

Warren Buffett's annual letters demonstrate this transparency principle. He explains exactly why Berkshire Hathaway bought or sold positions, acknowledges mistakes openly, and provides clear reasoning for capital allocation decisions. This level of communication should be standard, not exceptional.

Investors should expect detailed answers to these questions:

- What specific securities or positions does my portfolio hold?

- Why were these chosen over available alternatives?

- What conditions would trigger selling or rebalancing?

- How do fees compound over time and reduce my actual returns?

- What measurable results have similar strategies achieved historically?

Active Management Versus Passive Acceptance

The debate between active and passive management often misses the central point. The question isn't whether to be active or passive - it's whether your capital receives genuine attention or gets dumped into index funds regardless of valuation.

Research from Deloitte identifies technological innovation as a key trend reshaping wealth management. Yet technology alone doesn't create value. Active decision-making does.

When Bill Ackman publicly outlined his Pershing Square Holdings strategy during the 2020 market crash, he demonstrated what active management means: recognizing opportunity when fear dominates, acting decisively, and protecting capital when valuations become excessive. His firm hedged against market decline, then deployed capital aggressively when prices became attractive.

The Cost of Complacency

Understanding how inflation erodes purchasing power reveals why passive acceptance of modest returns guarantees wealth destruction. If your investments return 7% but inflation runs 5%, your real gain is only 2% - and that's before taxes and fees.

Real returns after inflation and taxes:

- Nominal return: 7%

- Inflation: 5%

- Taxes on gains (assume 20%): 1.4%

- Net real return: 0.6%

This math explains why many investors feel like they're running faster but staying in place. Their account balances grow nominally while purchasing power stagnates or declines.

Client Service Models That Actually Serve Clients

Examining the client engagement strategies of firms like revolve wealth partners shows movement toward more personalized service. The industry is slowly recognizing that treating clients as individuals rather than account numbers improves outcomes.

Stanley Druckenmiller, who delivered 30% annual returns at Duquesne Capital for three decades, credits his success to staying flexible and adapting to changing conditions. He didn't follow a rigid formula - he analyzed current opportunities and allocated capital accordingly.

Risk Profiles That Reflect Reality

Generic risk questionnaires asking whether you'd panic during a 20% decline don't capture what actually matters. Effective risk assessment considers:

- Your specific financial goals and timeline

- Current market valuations and economic conditions

- Your capacity to recover from losses (income, savings rate, time horizon)

- Actual emotional responses to previous market volatility

- The relationship between your wealth and your lifestyle requirements

Someone with $5 million who needs $100,000 annually has different risk parameters than someone with $500,000 needing the same income. Yet many advisors apply identical allocation models to both situations.

Generational Shifts in Wealth Management Expectations

Bridging generational differences in financial attitudes presents challenges for traditional firms. Younger investors demand different communication styles, technological integration, and philosophical approaches to wealth building.

Mark Zuckerberg's approach to capital allocation at Meta demonstrates how younger generations think differently about risk and returns. Rather than diversifying into safe, boring investments, he concentrates capital in areas where he has expertise and conviction - then manages those positions actively.

Generational preference differences:

| Baby Boomers | Millennials & Gen Z |

|---|---|

| Quarterly written reports | Real-time digital access |

| Phone call updates | App notifications and dashboards |

| Conservative diversification | Concentrated conviction bets |

| Long holding periods | Tactical flexibility |

| Relationship-focused | Results-focused |

This doesn't mean one generation is right and another wrong. It means wealth managers must adapt communication and strategies to match client preferences rather than forcing everyone into a single mold.

Technology Integration Without Losing the Human Element

Revolve wealth partners and other firms increasingly leverage technology for portfolio monitoring, rebalancing, and reporting. Yet the best firms recognize that algorithms can't replace human judgment during market extremes.

During the 2008 financial crisis, computers suggested buying financial stocks as they became statistically "cheap." Human analysts recognized the systemic risk and avoided catastrophic losses. During the 2020 pandemic crash, algorithms triggered panic selling at the bottom. Experienced managers recognized the opportunity.

For those interested in experiencing professional capital management before committing significant assets, Sovereign Prosperity's virtual trial allows you to observe real trading performance in a simulated environment without risking capital.

Fee Structures and Alignment of Interests

Traditional fee models create misaligned incentives. When advisors earn percentages of assets under management regardless of performance, they benefit from gathering assets even if returns disappoint. This explains why many firms focus on relationship-building rather than superior results.

Performance-based fees align interests better - managers only earn premium compensation when they deliver above-market returns. This structure dominated the hedge fund industry until it became mainstream enough that mediocre managers could gather assets through marketing rather than performance.

What Fee Transparency Actually Means

Investors should understand total cost of ownership:

- Direct advisory fees - What you pay the wealth manager

- Underlying fund expenses - Costs within mutual funds or ETFs

- Trading costs - Spreads and commissions on transactions

- Tax efficiency - How much return gets eaten by taxes

- Opportunity costs - Returns missed by holding cash or conservative positions

The average return illusion demonstrates why understanding these costs matters. A fund advertising 8% average returns might deliver only 5% to investors after all costs compound over time.

The Personalization Imperative

Cookie-cutter wealth management dies slowly because it's profitable for firms - one portfolio model serves hundreds of clients with minimal customization. But client expectations continue rising as investors recognize they deserve strategies matching their unique situations.

Cathie Wood's ARK Invest gained attention by creating highly specialized portfolios focused on specific innovation themes. While her performance has been volatile, the underlying principle resonates: investors want managers with deep conviction in particular strategies, not generic exposure to everything.

Elements of genuine personalization:

- Custom risk profiles based on actual financial situation

- Tax-loss harvesting tailored to your tax bracket

- Strategic cash reserves aligned with your liquidity needs

- Geographic and sector exposure matching your existing concentrations

- Rebalancing triggers customized to current market valuations

Due Diligence Questions for Wealth Management Firms

When evaluating firms like revolve wealth partners or any potential wealth management partner, asking the right questions reveals whether they'll genuinely serve your interests.

Essential questions to ask:

- What specific returns have you delivered after all fees over the past 5 and 10 years?

- How did your strategies perform during the 2020 crash and 2022 bear market?

- What percentage of your clients achieved their stated financial goals?

- How do you protect against inflation exceeding your returns?

- What would cause you to recommend I move capital elsewhere?

- How are you compensated, and what conflicts of interest exist?

- Can I speak with clients who have similar situations to mine?

The firms that answer these questions directly and specifically demonstrate confidence in their approach. Those that deflect into vague industry jargon or marketing language reveal absence of substance.

Performance Measurement That Matters

Absolute returns matter more than relative performance. Losing 15% when the market drops 20% provides no comfort - you still lost 15% of your wealth. Understanding what wealth actually means helps clarify that preserving and growing purchasing power matters far more than beating arbitrary benchmarks.

David Swensen at Yale's endowment focused on absolute returns needed to fund university operations, not on beating the S&P 500. This clarity of purpose guided every allocation decision and delivered superior long-term results.

Multi-Generational Wealth Preservation

Keeping wealth across generations requires more than investment management. It demands family education, governance structures, and philosophical alignment about money's purpose.

The Rockefeller family maintained wealth across six generations by institutionalizing family governance, education, and shared values. They didn't just pass down assets - they transferred the knowledge and discipline required to preserve and grow wealth responsibly.

Firms serving multi-generational clients should facilitate:

- Regular family meetings about wealth philosophy and goals

- Education programs for younger family members

- Succession planning that goes beyond legal documents

- Philanthropic structures that align family values

- Business succession strategies that preserve family harmony

The Future of Wealth Management

Industry trends for 2026 point toward continued disruption as technology enables new service models and client expectations evolve. Firms that adapt will thrive; those clinging to outdated approaches will gradually lose relevance.

The most significant shift isn't technological - it's philosophical. Investors increasingly recognize that traditional retirement planning based on 40-year wealth accumulation strategies may not deliver promised outcomes in an environment of persistent inflation and lower expected returns.

Active Capital Management for Accelerated Growth

Passive strategies work when markets consistently trend upward and inflation stays dormant. Today's environment rewards active management that recognizes when to be aggressive and when to be defensive. Understanding why banks prefer patient investors reveals how conventional wisdom often serves institutions rather than individuals.

Peter Lynch achieved 29% annual returns at Fidelity Magellan by staying actively engaged with markets, recognizing opportunities, and acting decisively. He didn't follow a passive formula - he adapted constantly to changing conditions.

The table below compares approaches:

| Factor | Passive Indexing | Active Management |

|---|---|---|

| Market awareness | Low - follows predetermined allocation | High - adjusts to conditions |

| Valuation sensitivity | None - buys regardless of price | Critical - seeks value |

| Risk management | Static diversification | Dynamic positioning |

| Inflation protection | Minimal - accepts market returns | Active - seeks real growth |

| Client customization | None - identical for everyone | High - matches individual needs |

Choosing Your Wealth Management Partner

Selecting who manages your capital ranks among life's most important decisions. The difference between a mediocre advisor and an excellent one compounds to millions of dollars over decades. Revolve wealth partners represents one option in a crowded field, but the principles for evaluation apply universally.

Look for firms that demonstrate:

- Transparent communication about strategies, fees, and results

- Active management that adapts to market conditions

- Alignment of interests through performance-based compensation

- Deep expertise in specific investment approaches

- Willingness to acknowledge limitations and mistakes

- Focus on real returns after inflation and taxes

The relationship matters as much as the strategy. Your wealth manager should challenge your assumptions, explain complex concepts clearly, and demonstrate genuine commitment to your success rather than their asset gathering.

The wealth management industry is evolving toward greater transparency, personalization, and active management as traditional passive approaches struggle to deliver real growth in inflationary environments. Understanding what differentiates effective firms from those following outdated models empowers you to make informed decisions about your capital. Sovereign Prosperity specializes in active capital management designed to outperform conventional strategies and deliver real wealth growth despite inflation. If you're ready to explore alternatives to traditional wealth management, start a conversation with us about how our approach might accelerate your path to financial independence.

This article was published by Tomas Vyšniauskas.

Click here to read more about the author.

Interested in applying these ideas?

Book a no-obligation consultation with our team to discuss your wealth goals.

More from Wealth Intelligence

Why Diversification Has Become a Financial Religion

Your Pension Might Be the Weirdest Deal You Ever Accept