Every bank, advisor, and wealth manager tells you the same thing: diversify. Somewhere along the way, that sound advice curdled into dogma - a belief system investors stopped questioning, even as it quietly delivered mediocre results.

A Tool Mistaken for a Goal

Diversification, used correctly, is genuinely useful. No serious investor wants their entire net worth riding on one fragile bet. Reducing unnecessary risk, preserving capital, building something sustainable - these are real goals worth pursuing.

The trouble starts when diversification stops being a tool and becomes the objective itself.

At Sovereign Prosperity, we see this constantly with ambitious professionals. They're doing everything "right": index funds, retirement accounts, mutual funds, bonds, some property, maybe a few alternatives sprinkled in. On paper, the portfolio looks sophisticated.

Zoom out, though, and a different picture forms.

They own a lot of things. They own very few exceptional things. Capital gets spread across so many average-return vehicles that real compounding slows to a crawl. Volatility drops - but so does upside, at almost the same rate.

That trade-off matters more than people realize, because life isn't infinite. Most ambitious professionals aren't optimizing for a decent portfolio at 85. They want meaningful wealth while they still have the energy, health, and freedom to use it.

Risk Reduction Is Not the Same as Diluting Opportunity

Picture this: you've identified three genuinely outstanding opportunities - investments you understand deeply, with real conviction behind them and asymmetric upside.

Then fear creeps in, and instead of allocating decisively, you spread that same capital across 25 positions because it "feels safer."

The result is predictable. Even if your best ideas perform brilliantly, their impact on your overall wealth gets diluted into irrelevance. You've protected yourself from volatility, but you've also engineered away the exceptional outcomes that were the entire point.

This is precisely what Charlie Munger spent decades pushing back on. Munger argued that wide diversification mainly makes sense for people unwilling - or unable - to think deeply about what they own. He called excessive diversification a hedge against ignorance.

That's blunt, but it holds up. If you don't understand what you own, broad diversification protects you from your own uncertainty, and that's rational. But if you have real expertise or access to superior opportunities, the same strategy starts costing you. Warren Buffett didn't build his fortune by owning hundreds of average businesses - he built it through concentrated bets on exceptional ones, made when conviction was high. That's not recklessness. It's selectivity.

What Eleven Years of Trading Taught Me

I learned a version of this lesson in trading, though not the way most people expect.

From 2010 to 2021, I worked my way through the trading world - price action, indicators, pattern systems, backtesting, probability models, retail courses. Like most people who enter financial markets, I assumed progress meant accumulating more: more strategies, more tools, more perspectives.

Looking back, that assumption was the problem. I was diversified in knowledge but had nothing close to mastery. My attention was scattered across too many frameworks and too many conflicting ideas to develop real depth in any of them - I was collecting intellectual clutter, not building a skill.

Everything changed in 2021, when I started learning under a real professional trader. The breakthrough didn't come from adding a tenth strategy to the pile. It came from stripping the pile down - dropping the conflicting frameworks and committing fully to one coherent model, studied at depth.

Progress accelerated the moment I diversified less. The same principle holds in investing: owning more doesn't automatically make you safer. Often it just makes you average - and in today's monetary environment, average comes with risks that don't show up on a statement. Inflation erodes it. Currency debasement erodes it. Time erodes it. A portfolio can look perfectly safe on paper while its real purchasing power quietly bleeds out.

People fear volatility so much that they'll happily accept stagnation instead. Stagnation carries its own risk - it's just slower and easier to ignore.

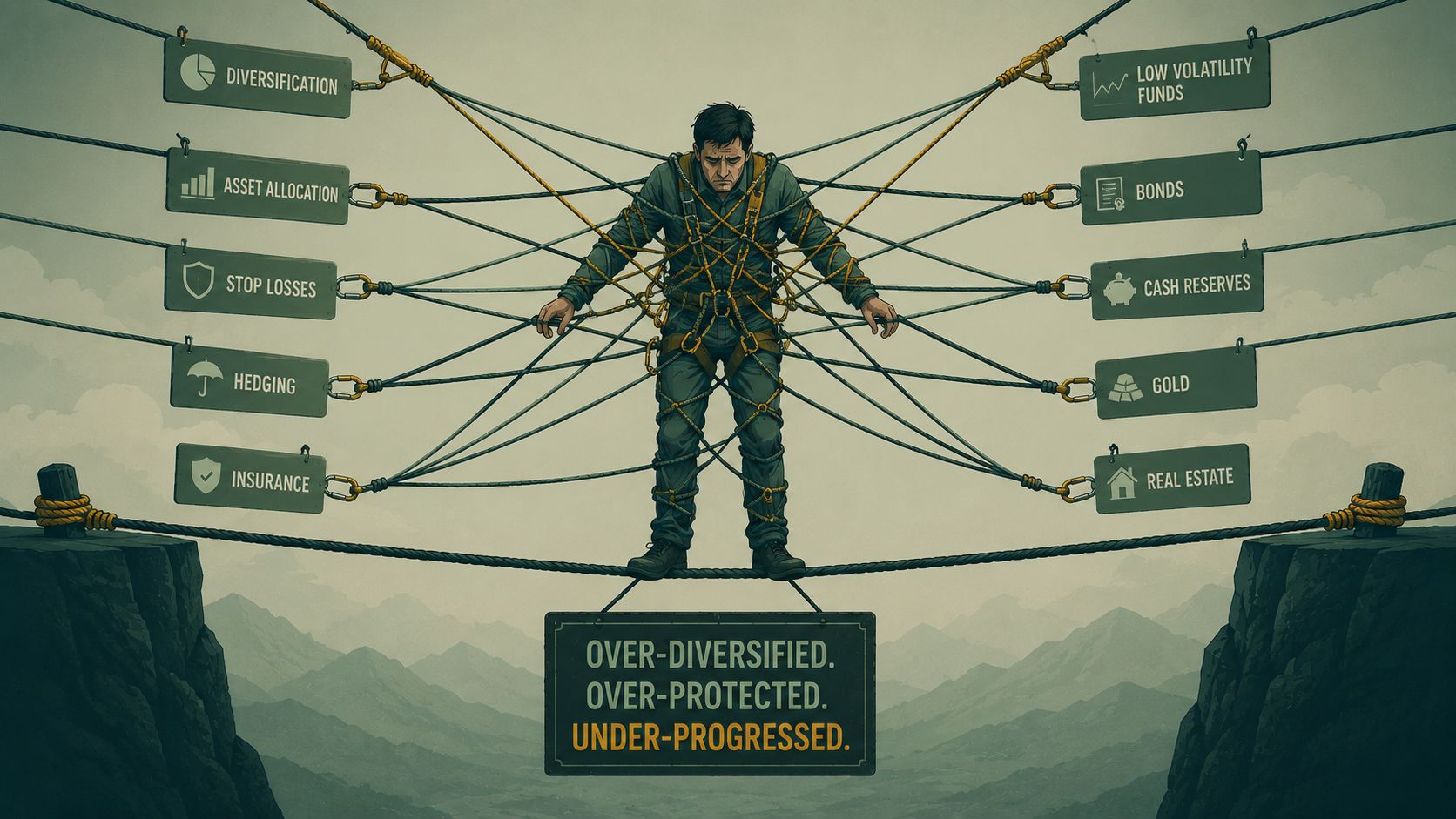

When Diversification Becomes Diworsification

The real question isn't whether diversification is good or bad. It's this: at what point does it stop protecting you and start working against you?

That tipping point has a name - diworsification. It happens when new positions stop meaningfully reducing risk and just keep eating into upside, usually because they were added for psychological comfort rather than strategic reason. At that point you're no longer allocating on conviction. You're allocating on fear, and fear is an expensive portfolio manager.

Take the standard portfolio built through conventional financial advice: index funds, some bonds, international exposure, a few sector ETFs, maybe REITs, maybe commodities, maybe cash. It reads as balanced on a spreadsheet.

In practice, many of these assets move together exactly when it matters most. When real stress hits markets, correlations spike, and the diversification that looked solid on paper turns out to have been complexity dressed up as resilience.

Stanley Druckenmiller made a related point about returns: the biggest gains rarely come from spreading bets thin. They come from being aggressive when conviction and opportunity actually line up. That's not a license for reckless betting - it's a reminder that extraordinary results come from extraordinary decisions, not averaged-out ones. The real skill is finding the balance: too much concentration breeds fragility, too much diversification breeds mediocrity, and the sweet spot sits between the two.

Five Questions to Test Your Portfolio

Here's a practical way to find out whether your portfolio is intelligently diversified or just diworsified.

Do I genuinely understand what I own? Many investors hold products they can barely explain - bought on a recommendation, a sophisticated-sounding name, or a compelling narrative. If you can't clearly state why you own something and what conditions make it work, that's a red flag.

Is this position meaningfully improving my portfolio? Every holding should do at least one of three things: increase expected return, reduce meaningful risk, or improve strategic flexibility. If it does none of those, it's dead weight.

Am I diversifying on logic or on fear? This might be the most important question of the five. Sometimes you already know where your best opportunities are, but fear talks you into diluting anyway because it feels safer. It rarely is.

Am I overestimating safety? Conventional investing treats low volatility as synonymous with safety, but real risk also includes permanent capital loss, eroding purchasing power, opportunity cost, and wasted time. A low-volatility portfolio that barely outpaces inflation isn't safe - it's slow erosion with better PR.

Does this portfolio actually match my life goals? A 35-year-old entrepreneur with strong income and high growth ambitions shouldn't be investing like a 68-year-old retiree focused purely on capital preservation. Conventional advice tends to treat every investor identically; your strategy should match your actual objective, not a generic template.

The Real Problem Isn't Income

There's a truth that doesn't get said often enough: most people don't have an income problem. They have a capital allocation problem. They work hard, earn well, and save consistently - yet their wealth grows slower than it should, because that capital sits in structures built for average outcomes.

Average outcomes tend to produce average lives.

At Sovereign Prosperity, we think wealth creation should be intentional - managed with clarity, aware of opportunity cost, respectful of risk, but equally respectful of time. Your best years matter, and they're happening now, not in some deferred future after decades of cautious accumulation. The goal isn't to postpone life while you wait to get rich. It's to build wealth intelligently enough that life and wealth move forward together.

That starts with asking a better question - not "how diversified am I?" but "is my capital working as intelligently as it could?"

Sometimes the biggest risk isn't concentration. It's spending decades comfortably average.

If conventional investing feels too slow, too passive, or too limited for what you're trying to build, it might be worth a different conversation. At Sovereign Prosperity, we work with serious individuals who want to approach wealth creation through professional capital management and a genuine long-term strategy. If that resonates, start a conversation with us.

Your future wealth may depend less on owning more things, and more on allocating what you have with real intelligence.

This article was published by Tomas Vyšniauskas.

Click here to read more about the author.

Interested in applying these ideas?

Book a no-obligation consultation with our team to discuss your wealth goals.

More from Wealth Intelligence

Why “Playing It Safe” Can Leave You Financially Vulnerable

Inflation Is the Invisible Tax Your Bank Never Talks About