Every financial decision you make today shapes your economic reality tomorrow. Most people approach wealth-building reactively, responding to market news, emotional impulses, or whatever financial product their bank happens to be promoting this quarter. The difference between those who achieve financial independence and those who remain trapped in the cycle of working for money comes down to one critical factor: a disciplined approach to making strategic capital decisions.

The Real Cost of Poor Financial Decision-Making

The average investor underperforms the S&P 500 by approximately 4% annually, according to decades of behavioral finance research. This performance gap isn't caused by lack of intelligence or access to information. It stems directly from flawed decision-making frameworks that prioritize short-term comfort over long-term wealth creation.

Consider the case of Warren Buffett's investment in Coca-Cola. In 1988, he made the financial decision to invest $1 billion in the company when most Wall Street analysts questioned the move. His framework wasn't based on quarterly earnings projections or market sentiment. Instead, he evaluated the company's competitive moat, management quality, and long-term brand strength. That single decision generated over $20 billion in value for Berkshire Hathaway shareholders.

The lesson isn't to copy Buffett's specific investments. It's to recognize that exceptional wealth creation requires a decision-making process fundamentally different from conventional thinking.

How Emotions Sabotage Wealth-Building Decisions

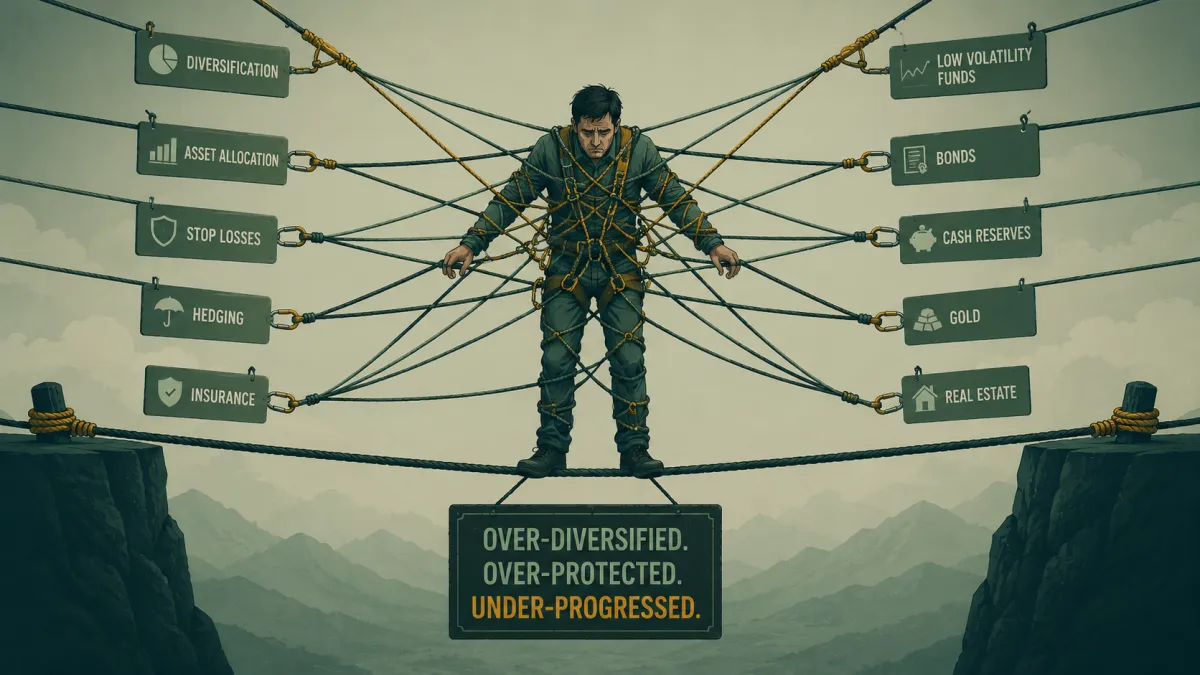

Every financial decision carries an emotional component that most people fail to recognize until it's too late. Fear drives investors to sell near market bottoms. Greed pushes them to chase performance at market peaks. Regret causes them to avoid necessary risks after previous losses.

Ray Dalio built Bridgewater Associates into the world's largest hedge fund by creating systematic decision-making processes that removed emotional bias. His "Principles" approach treats investment decisions as exercises in probabilistic thinking rather than gut feelings. When markets crashed in 2008, while others panicked, Bridgewater's systematic approach allowed them to navigate the crisis profitably.

Key emotional traps that destroy wealth:

- Anchoring bias: Fixating on purchase prices rather than current value and future potential

- Confirmation bias: Seeking information that validates existing beliefs while ignoring contradictory evidence

- Recency bias: Overweighting recent events when evaluating long-term trends

- Loss aversion: Feeling losses twice as intensely as equivalent gains, leading to overly conservative positioning

The Consumer Financial Protection Bureau emphasizes that developing strong financial decision-making skills requires both knowledge acquisition and emotional discipline.

Building a Strategic Framework for Capital Decisions

A robust financial decision-making framework transforms wealth-building from gambling into engineering. You need clear criteria, measurable outcomes, and systematic processes that work regardless of market conditions.

The Three-Layer Decision Model

Layer 1: Strategic Allocation - This foundational layer determines how you allocate capital across different asset classes and strategies. Your decisions here should align with your wealth-building timeline, risk capacity, and financial independence goals. Unlike traditional portfolio allocation that prioritizes "balance," strategic allocation focuses on growth vehicles that can actually change your economic position.

Layer 2: Tactical Positioning - Within your strategic framework, tactical decisions respond to changing market conditions and opportunities. This isn't market timing. It's intelligent positioning based on valuation, risk-reward ratios, and probability-weighted outcomes.

Layer 3: Risk Management - Every financial decision must incorporate downside protection. This layer ensures that even when individual decisions prove wrong, your overall wealth trajectory remains intact.

| Decision Layer | Time Horizon | Primary Objective | Review Frequency |

|---|---|---|---|

| Strategic Allocation | 3-5+ years | Wealth creation | Annually |

| Tactical Positioning | 6-24 months | Opportunity capture | Quarterly |

| Risk Management | Ongoing | Capital preservation | Monthly |

Consider how Mark Cuban approached financial decision-making when selling Broadcast.com to Yahoo for $5.7 billion in stock during the dot-com bubble. While others criticized his immediate decision to hedge the position through protective options strategies, Cuban understood that protecting his wealth was more important than maximizing theoretical upside. When the bubble burst, his systematic risk management preserved hundreds of millions in wealth that others lost.

Common Financial Decision Mistakes That Keep People Stuck

Most individuals make the same predictable mistakes when approaching major financial decisions. Recognizing these patterns allows you to avoid them systematically.

Mistake 1: Optimizing for Tax Efficiency Instead of Wealth Creation

Tax considerations should inform financial decisions, but they shouldn't dominate them. Too many investors hold underperforming assets for years to avoid capital gains taxes, destroying far more wealth through opportunity cost than they save in taxes.

The mathematics are straightforward: if you're holding an asset returning 3% annually to avoid a 20% capital gains tax, but alternative investments could return 10% annually, you're making a terrible financial decision. You'd pay $20,000 in taxes on a $100,000 gain but could generate $7,000 in additional annual returns ($10,000 vs. $3,000) moving forward.

Mistake 2: Following Conventional Timeline-Based Advice

Traditional financial planning tells 30-year-olds to accept 6-7% annual returns because "time is on their side." This advice serves financial institutions, not wealth-builders. Understanding why banks promote patient investing reveals how conventional timeline thinking keeps most people from achieving real financial independence.

The timeline fallacy breaks down when you run the numbers:

- 6% annual returns on $50,000 over 30 years: $287,175

- 12% annual returns on $50,000 over 30 years: $1,497,996

- 18% annual returns on $50,000 over 30 years: $7,178,039

Every percentage point matters enormously over time. The financial decision to accept mediocre returns because you're young isn't conservative - it's economically devastating.

Mistake 3: Confusing Activity with Progress

Many investors make constant financial decisions - trading frequently, rebalancing obsessively, chasing new opportunities - while generating minimal wealth creation. Charlie Munger famously said that Berkshire Hathaway's success came from "sitting on our asses" while great businesses compounded.

Stanford's Initiative for Financial Decision-Making researches how individuals can improve their financial choices through better frameworks rather than increased activity.

Decision-Making Under Uncertainty: The Real World

Financial decisions never occur with perfect information. Markets are inherently uncertain. Economic conditions change. Unexpected events disrupt even the most carefully constructed plans.

The key question isn't how to eliminate uncertainty - that's impossible. The question is how to make excellent financial decisions despite uncertainty.

Probabilistic Thinking for Wealth Builders

Instead of asking "Will this investment work?" ask "What's the probability distribution of outcomes, and what's my expected value across that distribution?"

When Jeff Bezos made the financial decision to invest in Blue Origin, he wasn't certain of success. He structured the decision around acceptable loss - capital he could deploy toward a high-potential, high-uncertainty venture without jeopardizing his core wealth. That's sophisticated decision-making.

Probabilistic decision framework:

- Identify the range of possible outcomes

- Assign rough probabilities to each scenario

- Calculate expected value across scenarios

- Determine acceptable loss if worst-case occurs

- Size position accordingly

This approach transforms financial decision-making from binary yes/no choices into nuanced risk-reward optimization.

Information Quality Versus Information Quantity

The explosion of financial information hasn't improved decision quality for most investors. More data creates more noise, making it harder to identify signal. Research on cognitive attributes in financial decision-making shows how information processing patterns significantly impact outcomes.

The best financial decision-makers consume less information but higher quality inputs. They focus on fundamental drivers rather than daily noise. They build knowledge that compounds rather than collecting facts that depreciate.

Practical Implementation: From Framework to Action

Understanding financial decision-making principles doesn't create wealth. Implementation does. Here's how to translate framework into results.

Step 1: Define Your Wealth-Building Objectives

Calculating your "enough number" provides clarity that improves every subsequent financial decision. When you know your target, you can work backward to determine required returns, acceptable risks, and necessary capital deployment.

Vague goals like "build wealth" or "retire comfortably" don't enable strategic decision-making. Specific targets like "accumulate $5 million in investable assets within 15 years" create measurable milestones and accountability.

Step 2: Establish Decision Criteria

Write down your specific criteria for major financial decisions before you need to make them. This pre-commitment prevents emotional decision-making during stressful moments.

Example criteria set:

- Minimum expected annual return: 12%

- Maximum single-position risk: 15% of portfolio

- Required liquidity timeline: Ability to exit within 30 days

- Inflation protection: Returns must exceed inflation by at least 5%

- Complexity threshold: Must understand investment thesis in under 10 minutes

Step 3: Create Your Decision Journal

Document every significant financial decision - the rationale, expected outcome, actual result, and lessons learned. This practice creates a feedback loop that systematically improves decision quality over time.

Paul Tudor Jones, the legendary hedge fund manager, maintains detailed trading journals analyzing both winning and losing positions. This systematic review process helped him identify patterns in his decision-making that he could optimize or eliminate.

| Decision Date | Action Taken | Rationale | 6-Month Outcome | Key Lesson |

|---|---|---|---|---|

| Jan 15, 2026 | Increased equity exposure | Valuation opportunity | +8.3% return | Timing was early but direction correct |

| Mar 3, 2026 | Exited bond position | Rising rate environment | Avoided -4.1% loss | Macro analysis proved accurate |

Advanced Considerations for Serious Wealth Builders

Once you've established fundamental decision-making discipline, advanced techniques can further optimize wealth creation.

Capital Efficiency and Opportunity Cost

Every dollar you deploy carries an opportunity cost - the return you sacrifice by choosing one investment over alternatives. Understanding inflation's impact on wealth highlights why seemingly "safe" decisions often carry enormous hidden costs.

The financial decision to hold cash earning 2% in a 4% inflation environment doesn't feel risky, but you're systematically destroying purchasing power. That's a terrible decision disguised as prudence.

Leverage and Risk Asymmetry

Sophisticated investors understand that strategic leverage - when applied with proper risk controls - can dramatically accelerate wealth creation. The key word is "strategic." Reckless leverage destroys capital. Intelligent leverage amplifies returns while maintaining downside protection.

Stanley Druckenmiller built his fortune by making concentrated bets when he identified high-probability opportunities with asymmetric risk-reward profiles. His financial decision-making process involved using leverage during periods of high conviction while maintaining strict risk management that prevented any single loss from becoming catastrophic.

The Active Management Advantage

Passive investment strategies have been marketed as the optimal financial decision for retail investors. This narrative serves large financial institutions beautifully - it generates predictable fee streams while requiring minimal effort.

For investors seeking accelerated wealth creation, active capital management offers superior potential when executed with discipline and expertise. The Starter Tier at Sovereign Prosperity demonstrates how professional capital management can be accessible starting from $2,000, providing an alternative to conventional passive approaches.

The data shows that skilled active managers consistently outperform during volatile periods and market transitions - exactly when passive investors suffer most. Your financial decision shouldn't be active versus passive. It should be: "Do I have access to genuinely skilled active management that justifies the difference in approach?"

Building Decision-Making Skills Over Time

Financial decision-making ability improves with deliberate practice and systematic learning. Research on financial decision-making development demonstrates that structured processes enhance outcomes across all experience levels.

Learning from Wins and Losses

Every financial decision provides data. Winners teach you what works. Losers teach you what to avoid. The key is extracting maximum learning from both.

When George Soros made his famous financial decision to short the British pound in 1992, generating over $1 billion in profit, he wasn't lucky. He spent months analyzing the structural problems with Britain's currency peg, evaluating probability of political responses, and sizing his position accordingly. That single decision reflected decades of developed expertise.

Course Correction Without Emotional Attachment

The ability to recognize when a financial decision isn't working and course-correct quickly separates professional wealth builders from amateurs. Exploring the various types and techniques of financial decision-making reveals how systematic approaches enable faster, less emotional adjustments.

Peter Lynch's success at Fidelity Magellan Fund came partly from his willingness to sell positions quickly when his original thesis proved wrong. He didn't average down on losing positions or hold them hoping for recovery. He reassessed, made new decisions based on current reality, and moved capital to better opportunities.

The Compounding Effect of Better Decisions

Small improvements in financial decision quality compound dramatically over time. A 2% improvement in annual returns might seem insignificant, but over 20 years it transforms outcomes.

The mathematics of decision quality:

- Average decision quality (8% annual return): $100,000 becomes $466,096

- Slightly better decisions (10% annual return): $100,000 becomes $672,750

- Significantly better decisions (12% annual return): $100,000 becomes $964,629

- Exceptional decisions (15% annual return): $100,000 becomes $1,636,654

The difference between average and exceptional financial decision-making is nearly $1.2 million on a $100,000 starting position over 20 years. That gap represents freedom, security, and options that compound across every area of life.

Understanding the wealth gap between employees and owners illuminates how systematic capital decisions create exponentially different financial outcomes over career spans.

Making Your Next Decision Count

Financial decision-making isn't abstract theory. It's the practical application of frameworks that either build wealth or waste time. Every capital allocation, every risk assessment, every strategic choice moves you closer to or further from financial independence.

The individuals who achieve meaningful wealth don't possess secret information or special advantages. They apply better decision-making frameworks consistently over time. They optimize for long-term value creation rather than short-term comfort. They understand that aligning decisions with clear financial goals creates measurable progress toward specific outcomes.

Your wealth trajectory over the next decade will be determined primarily by the financial decisions you make in the next 12 months. Choose your framework carefully. Implement systematically. Course-correct quickly when needed.

Exceptional wealth creation starts with exceptional decision-making, but even the best framework requires skilled execution and disciplined implementation. If you're serious about accelerating your path to financial independence through active capital management that outperforms traditional approaches, Sovereign Prosperity offers strategic alternatives designed for individuals who value real growth over conventional thinking. Start a conversation with us today about building a wealth management approach aligned with your specific objectives and timeline.

This article was published by Tomas Vyšniauskas.

Click here to read more about the author.

Interested in applying these ideas?

Book a no-obligation consultation with our team to discuss your wealth goals.

More from Wealth Intelligence

The Wealth Trap of Extreme Delayed Gratification

Your Pension Might Be the Weirdest Deal You Ever Accept