For decades, millions of Europeans have believed in a simple promise: work hard, pay your taxes, and the state will take care of you in retirement. That promise is quietly breaking down - and most people haven't noticed yet.

The pension promise depends entirely on demographics cooperating - and they've stopped.

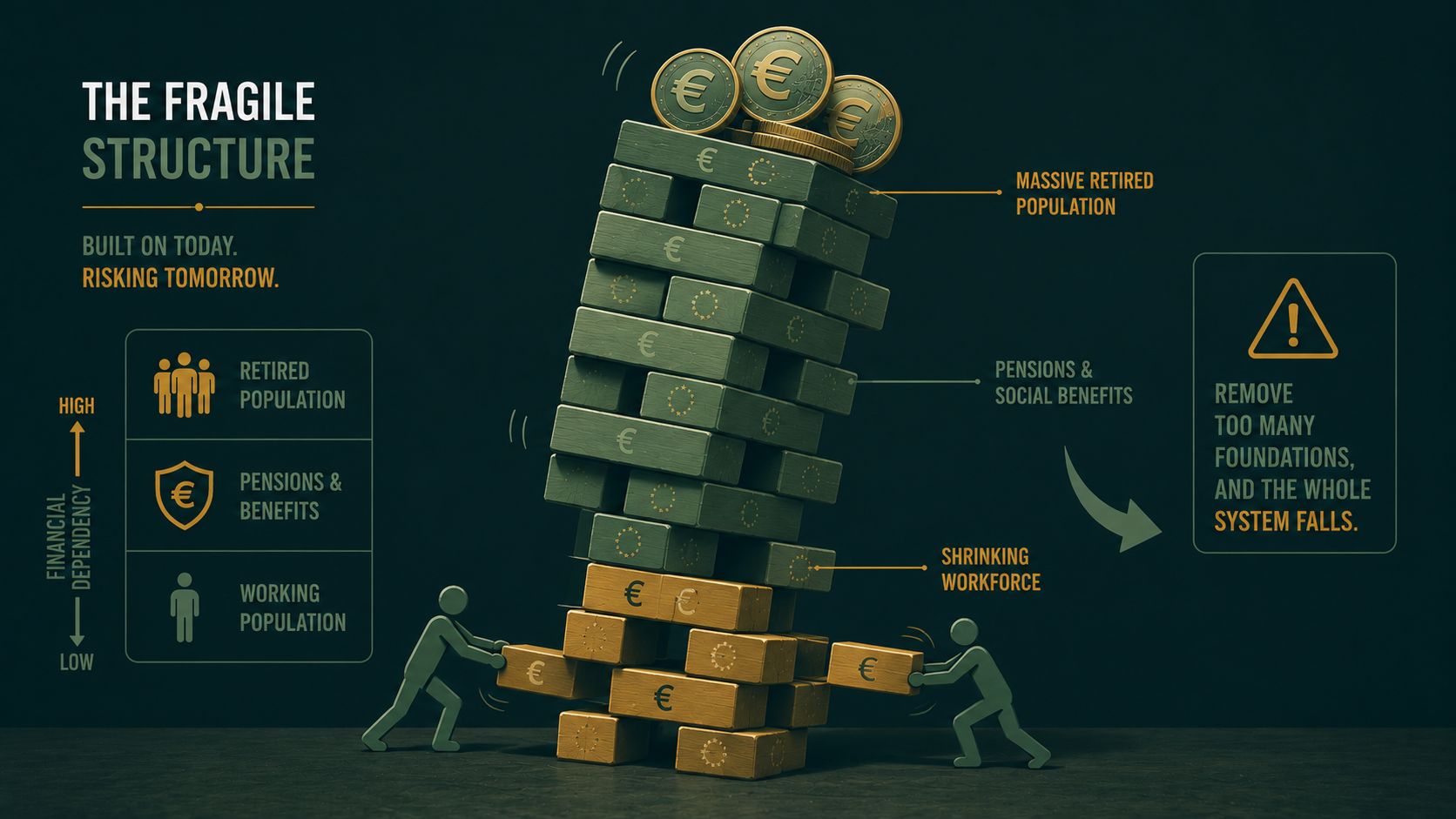

For most of modern European history, the system worked because the math worked. Large working populations supported smaller retired populations, governments collected contributions, redistributed them, and kept up the appearance of long-term stability. That stability is now under real pressure.

Europe is aging fast. Birth rates are falling, life expectancy is rising, and together those forces are quietly reshaping retirement economics. The problem isn't complicated: more retirees, fewer workers, greater strain on the system trying to support them.

In many European countries, the worker-to-retiree ratio keeps deteriorating year after year. Decades ago, several workers supported each retiree. Today that cushion is shrinking fast, and in some regions we're heading toward a future where two workers - or fewer - effectively support one pensioner.

Pensions are usually discussed as though they're guaranteed assets sitting in a vault somewhere with your name on them. They're not. Most state pension systems are promises backed by future tax revenue and future political decisions - and that distinction matters more than most people realize.

The Quiet Retirement Crisis Already Exists

Many people imagine pension risk as some distant future problem. It isn't. For millions of retirees across Europe, the crisis is already here - it just doesn't look dramatic enough to make headlines.

It looks like an elderly couple in Germany turning down the heating in winter to save on bills. It looks like a retiree in France cutting back on groceries once rent and energy are paid. It looks like pensioners in Italy leaning heavily on their children just to get by. No collapse, no panic, no dramatic headline - just a slow erosion of financial dignity.

This is the kind of risk most people fail to respect, precisely because it happens gradually. But gradual problems compound, and over years they can become devastating. At Sovereign Prosperity, we keep coming back to a principle most investors underestimate: slow risk can be more dangerous than fast risk. Fast risk triggers alarm. Slow risk gets tolerated right up until it becomes painful - and pension fragility belongs firmly in that second category.

Inflation Changes the Retirement Equation

Even if pensions pay out exactly as promised, there's another problem most people underestimate: purchasing power. This might be the most important part of the whole discussion, because retirement isn't really about nominal income - it's about what that income can actually buy.

A €2,000 monthly pension sounds fine in isolation. The real question is what €2,000 will buy in 10, 20, or 30 years. That's where the illusion begins.

Most people think about inflation through official government numbers, but real-world inflation is far more personal - and a retiree's inflation is often worse than the headline figure, because retirees spend disproportionately on the categories that tend to rise the fastest: housing, utilities, healthcare, food, insurance. The essentials.

At Sovereign Prosperity, we often point out that official inflation figures can be technically accurate while still being practically misleading. Averages hide reality. The inflation an elderly person feels while heating a home in winter can look nothing like the headline CPI number, which means even a "stable" pension can quietly weaken over time. You keep receiving the same payment - but your standard of living deteriorates anyway.

The Hidden Risk of Dependence

This is where ambitious professionals should really pay attention. The greatest pension risk isn't lower payouts - it's dependency: on government policy, on demographics, on political decisions, on systems you don't control. That dependency creates vulnerability, and vulnerability reduces freedom.

Here's the uncomfortable part: many high-performing professionals spend decades building successful careers while outsourcing their entire retirement to institutions. That's dangerous, because no government cares about your retirement as much as you do, and no politician will ever prioritize your personal financial freedom over their political incentives. Relying primarily on a pension isn't financial planning. It's passive hope - and hope isn't a strategy.

Even the Wealthy Can Miscalculate

This illusion isn't limited to average workers - even hugely successful people misjudge long-term financial security. Mike Tyson earned hundreds of millions over his career and still ended up in financial collapse. Boris Becker earned vast sums and later faced severe financial trouble of his own. Different causes, same lesson: large earnings don't guarantee long-term security. What matters is how the capital is managed.

Income matters. Capital allocation matters more. That's true whether you earn €50,000 a year or €5 million - without intelligent capital management, financial security stays surprisingly fragile.

My Own Realization

I came to a similar conclusion through a different route. For years I worked inside the financial world searching for answers, and like most people, I initially trusted the conventional script because it sounded logical: study hard, work hard, save consistently, invest conventionally, wait patiently. It sounds safe.

Over time, though, I started seeing the cracks. The traditional financial world is full of narratives that look rational on the surface while quietly hiding major weaknesses - and once I noticed that, I couldn't unsee it.

Later, after spending 11 years learning trading the wrong way, I found Robert Taylor, one of the few genuinely sharp professionals I'd encountered. His understanding of markets was nothing like what the retail world teaches, and one lesson stuck with me: real wealth creation requires understanding reality as it actually is, not as convenient narratives present it. That applies to trading, and it applies just as much to retirement planning.

The pension narrative is one of those convenient narratives - comforting, simple, widely accepted, and increasingly detached from reality.

What Smart Professionals Should Do Instead

None of this means pensions are worthless - they can still play a useful role. But they should be treated as one layer of retirement security, not the foundation. A more intelligent framework looks like this:

1. Assume your pension will be insufficient

This single mindset shift changes behavior immediately. Plan as though your pension will help but won't fully protect your lifestyle, and you create a healthier sense of urgency around the rest of your planning.

2. Build capital aggressively during your peak earning years

Your 30s, 40s, and 50s matter enormously - these decades are your greatest opportunity to build meaningful capital, and wasting them on overly conservative strategies can be expensive.

3. Focus on real returns, not nominal ones

A portfolio returning 6-8% sounds respectable, but if inflation and currency debasement are quietly eating into purchasing power, real progress can be disappointing. Keep asking yourself: am I genuinely growing wealth in real terms, or just watching numbers go up?

4. Prioritize intelligent capital allocation

Working harder has its limits; scaling capital intelligently doesn't. This is where sophisticated wealth-building becomes powerful - not reckless speculation, not passive stagnation, but disciplined risk, intelligent positioning, and long-term growth.

Retirement Should Mean Freedom, Not Survival

The deeper issue here isn't really pensions - it's quality of life. Retirement should mean freedom: to travel, to spend time with family, to enjoy life with dignity. Not survival, not anxiety, not quiet dependence on a system you never controlled.

At Sovereign Prosperity, we believe wealth should serve life, not consume it. The goal isn't to spend 40 years postponing life in the hope that everything eventually works out - it's to build wealth intelligently so life can actually be enjoyed along the way. Maybe the greatest risk isn't market volatility at all. Maybe it's quietly trusting a retirement system that may never deliver what you expect.

If this article challenged how you think about retirement, good - the right questions can change a financial trajectory. If you're an ambitious professional who wants to build wealth more intelligently, faster than conventional approaches but still sustainably and responsibly, start a conversation with Sovereign Prosperity. Ask questions. Challenge assumptions. Understand our philosophy.

One intelligent decision today can meaningfully change your future. And your future deserves more than passive hope.

This article was published by Tomas Vyšniauskas.

Click here to read more about the author.

Interested in applying these ideas?

Book a no-obligation consultation with our team to discuss your wealth goals.

More from Wealth Intelligence

The 40-Year Wealth Plan: Why Your Retirement Strategy May Be Built on an Empty Promise

Why “Playing It Safe” Can Leave You Financially Vulnerable